Definition

Demand refers to consumers’ willingness to purchase goods and services at given prices. [1]

The Law of Demand states that quantity purchased varies inversely with price. The higher the price, the lower the quantity demanded. [2]

A demand curve (more formally known as a demand schedule) is a mathematical function or graphical representation of the quantity demanded for a product at different prices, all other things being equal. [3]

Demand schedules are used in marketing to help determine the price point for a product given sales and margin goals.

Although it is customary for P to appear on the Y-axis and Q on the X-axis in economics textbooks, it is also the usual practice in science to represent the independent variable (price, in this case) on the horizontal (X) axis. [1]

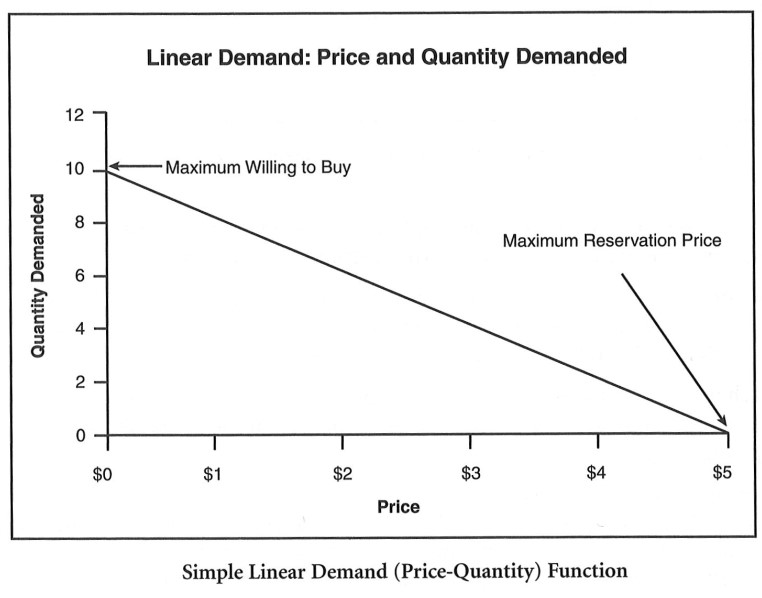

Linear demand occurs when each increment in price reduces the quantity consumers are willing to purchase by an equal amount. [4]

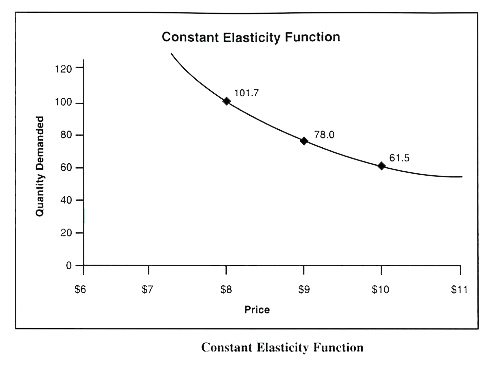

A constant elasticity demand curve has a constantly changing slope with the underlying assumption that a small percentage change in price causes the same percentage change in quantity, regardless of the initial price. [4]

A demand curve can be shifted outward by increasing brand preference. Management can then choose to sell the same quantity of branded products at a higher price, a higher quantity at the same price, or some other combination of these along the new demand curve. [4] (see MASB video: Five Compelling Reasons for Brand Preference)

Related Concepts

Maximum Reservation Price: The lowest price at which quantity demanded equals zero. Above this price, no customer will buy the product.

Maximum Willingness to Buy: The quantity that customers will “buy” when the price of a product is zero. This artificial concept is used to anchor a linear demand function.

See Also

Demand analysis

Demand areas

Demand density

Demand factors

Demand-oriented pricing

References

- Common Language in Marketing Project, 2021.

- Investopedia.com

- Paul A. Samuelson, Economics: An Introductory Analysis; New York, 1967; pg 59.

- Farris, Paul W., Neil T. Bendle, Phillip E. Pfeifer, & David J. Reibstein (2010). Marketing Metrics: The Definitive Guide to Measuring Marketing Performance (Second Edition). Upper Saddle River, New Jersey: Pearson Education, Inc.